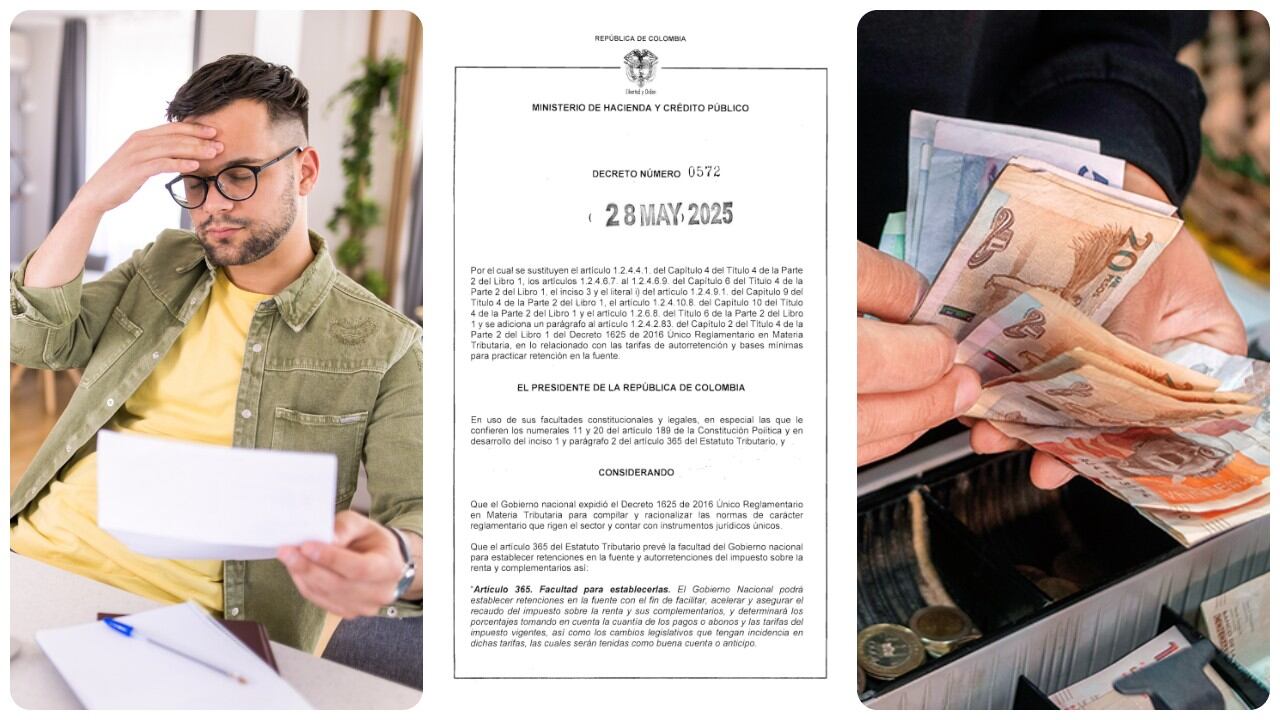

Although began to govern since June 1, the new decree that modified the retention rates at the source and self -retention, issued by the Ministry of Finance, does not stop causing stupor among the headdresses; and the norm already has even a lawsuit filed before the State Council.

Most sectors complain that their box will greatly affect and criticisms rainto the point that some have in mind that as wage earners they could also be touched with the changes, which, of course, is not so.

In general, The controversy has focused on the increase for some economic activitieswithout delving into several truths that have been counted.

A couple of experts analyzed some of the circumstances of this decree.

1. Retention and self -retention, what is the distance?

Table of Contents

The decree issued refers to an increase in retention rates at the source and changes in self -retention. What does it imply?

The self -retention is when the company pays a percentage of its own income and records that money to the DIAN. Meanwhile, the retention occurs when the company discounts a percentage to another third, whether employee or supplier, and then transfers that money to the DIAN.

2. Now there are more obliged

Although many of the studies around the taxes suggest that all citizens of a country should contribute something, since it is a matter of equity, since all use the goods and services that are carried out with the tax collection, Miguel Ángel Fandiño, tax director of the PWC Colombia firm, points out, first, what is the true nature of the retention in the source.

“Categorically it can be affirmed that retention at the source is not a taxnor can it be conceptually confused with him, although his values, both that of retention and the income tax in charge, may eventually coincide. ”

According to the expert, “the retention made on the income paid or paid in account is a collection mechanism, perhaps the main method of collection of income tax, but of course it is not the same tax. The truth is that they can coincide, but a retention rate cannot be set that overflows in its collection of the tax in chargeunder penalty of violating the content of the legal rank provisions, as well as the constitutional postulates that guide the tax system ”.

Modify retention rates at the source although it can be done from the government, we must not forget that this advance “The purpose of gradually achieves that the tax is collected – in the possible – within the same taxable year in which it is caused (Article 367 of the Tax Statute). Therefore, it is not subject to the arbitration that the Executive can freely set. ”

Juan Pablo Suárez, leading Taxer of CMM Legal Study, explains three changes that will make many more Colombians end up paying more. The first is the reduction of thresholds. “For example, before the payments for service provision only forced to practice retention at the source, if the payment was less than 4 UVT ($ 199,196); now, retention must be practiced for any payment above 2 UVT ($ 99,598). Another example is the acquisition of goods or agricultural products, where the threshold passed from 90 UVT to 70 UVTs,” he says.

The second, is the increase in rates, because “higher rates of self -retention (up to 4.5%) are imposed according to the economic sector. The comparative of the rates before and then is very telling.” And the third. It is the elimination of benefits. “Exemptions of payments are limited that were not subject to retention, such as agricultural purchases and CDAT,” he explained.

3. Inexplicable Differences

To some economic activities, through the issued decree, they are increased more than double what they had with the pre-form rates.

According to Fandiño, “An absence is evidenced in the motivation of the decree For the vast majority of economic activities that are affected with this increase, without any support at the technical level. ”

Worse, for the expert, the new standard has serious errors, as highlighted. “List economic activities that are typical of those qualified as non -taxpayers, which, due to their essence, have the condition of non -contributors, for example business associations, political, religious associations, of employees, among others ”.

4. The most ‘nailed’

Jeisson Ramírez, director of the Touché Advisors firmhe states that, from their perspective, “sectors that provide services or sell goods by values close to the minimum retention base, which, in addition, was changed (now is lower, confirming that new obligated people) would be affected.”

Ramírez set the example of the services sector, which was left with a basis to enter among those forced, 2 UVT (tax value unit), which is equivalent to 100,000 pesos. This means that whoever provides a service for 110,000 pesos, at the time of paying will be deducted the retention at the source, explained the expert.

As strongly affected groups, Ramírez makes the case in the real estate sector, which went from a rate of 1.1 % on income, at a rate of 3.5 %.

5. To those who cannot force them to self -retention

In Colombia it is common for companies to be created They have no employees, because they start as an entrepreneurship that does not give margin to hire labor.

In those cases, if the company has no employees, it would not be obliged to declare the self -retention of the new decree.