Elderly Man Convicted in Norway for Extensive Financial Crimes

Table of Contents

- Elderly Man Convicted in Norway for Extensive Financial Crimes

- Unmasking Financial Crime: The Rise of Invoice Fraud and Money Laundering

- Unmasking the Sophisticated Web of Invoice Fraud: A Deep Dive

- Cracking Down on Invoice Fraud: A Deep Dive into Recent Cases and Prevention Strategies

- Unmasking Invoice Factories: A Deep Dive into financial Crime

- Invoice Factory kingpin Convicted: Unpacking the Modus Operandi and Legal Fallout

- Debate Over Severity of Punishment in Adultery case involving Financial Impropriety

- Supreme Court Upholds Conviction in Fictitious Invoicing Case: A Landmark Decision

- Sophisticated Money Laundering Schemes Alarm Authorities

Published: by Archnetys News

fraudulent Invoicing Scheme Uncovered

A man in his seventies has been found guilty by the Buskerud District Court in Norway for orchestrating a significant financial fraud. The charges include aggravated financial infidelity amounting to approximately NOK 8 million, alongside serious money laundering of around NOK 1.2 million, and severe accounting irregularities.

Details of the Deception

The core of the scheme involved the creation and sale of fraudulent invoices to companies within the building and construction sector. These invoices purported to be for services such as painting and brushing work. However, investigations revealed that none of these services were ever rendered.This type of fraud is not uncommon; according to a recent report by the Norwegian National Authority for Examination and Prosecution of Economic and Environmental Crime (ØKOKRIM),invoice fraud accounts for nearly 20% of all reported financial crimes in the construction industry.

Accusation and Defense

While the defendant has acknowledged the factual basis of the accusations against him, he maintains that the imposed penalty is excessively harsh. The court, however, determined that the scale and purposeful nature of the fraud warranted the sentence.

“The defendant’s actions demonstrated a clear intent to deceive and profit unlawfully at the expense of legitimate businesses,” stated the presiding judge during the sentencing.

impact on the construction Industry

Financial crimes like these can have a ripple effect, impacting not only the companies directly targeted but also the overall stability and trustworthiness of the construction industry. Such fraudulent activities can led to increased costs for consumers and undermine fair competition.

As Openness International

notes, the construction sector is notably vulnerable to corruption and fraud due to the complex nature of projects and the large sums of money involved.

Legal Repercussions and Future Implications

The conviction serves as a stark reminder of the legal consequences awaiting those who engage in financial fraud. Authorities are increasingly vigilant in detecting and prosecuting such crimes, employing advanced data analytics and investigative techniques to uncover illicit activities.

Unmasking Financial Crime: The Rise of Invoice Fraud and Money Laundering

Published: by Archynetys.com

A deep dive into the escalating problem of invoice fraud, its connection to money laundering, and the measures being taken to combat these complex financial crimes.

The Insidious Spread of Invoice Fraud

Invoice fraud, a deceptive scheme involving falsified or manipulated invoices, is becoming an increasingly prevalent method for criminals to illicitly transfer funds and launder money. This type of fraud frequently enough involves creating fake invoices for services or goods that were never actually provided, or inflating the value of legitimate invoices. The proceeds from these fraudulent invoices are then channeled through various accounts to obscure their origin, making it arduous for law enforcement to trace the funds back to the criminal activity.

This invoice is false. it shows NOK 100,000 for painting work that has never been done.

Photo: Økokrim

The simplicity and adaptability of invoice fraud make it a favored method for money laundering. Unlike more complex schemes, it can be executed wiht minimal infrastructure and can be easily adapted to different industries and business models. This versatility allows criminals to exploit vulnerabilities in accounting systems and internal controls, making detection challenging.

The Link Between Invoice Fraud and Money Laundering

Money laundering, the process of concealing the origins of illegally obtained money, often relies on complex financial transactions to obscure the source of funds.Invoice fraud provides a seemingly legitimate way to introduce illicit funds into the financial system. By creating fake invoices, criminals can justify the transfer of money from one account to another, making it appear as a genuine business transaction.

Once the funds are laundered through invoice fraud, they can be used to finance further criminal activities, such as drug trafficking, terrorism, and human trafficking.The interconnectedness of these crimes highlights the urgent need for effective measures to combat invoice fraud and money laundering.

Combating Financial crime: Strategies and Solutions

Addressing the growing threat of invoice fraud and money laundering requires a multi-faceted approach involving collaboration between financial institutions, law enforcement agencies, and regulatory bodies. Some key strategies include:

- Enhanced Due Diligence: Financial institutions must implement robust due diligence procedures to verify the legitimacy of invoices and the identities of the parties involved in transactions.

- Advanced analytics: Utilizing data analytics and artificial intelligence to identify suspicious patterns and anomalies in financial transactions can help detect invoice fraud schemes.

- Employee Training: Educating employees about the red flags of invoice fraud and money laundering can empower them to identify and report suspicious activity.

- Regulatory Oversight: Strengthening regulatory frameworks and increasing oversight of financial institutions can definitely help deter and detect financial crimes.

- International Cooperation: Collaborating with international partners to share details and coordinate investigations is crucial for combating cross-border financial crimes.

By implementing these strategies, we can create a more secure and transparent financial system, making it more difficult for criminals to exploit vulnerabilities and launder money through invoice fraud.

Unmasking the Sophisticated Web of Invoice Fraud: A Deep Dive

Published:

The rising Tide of Deceptive Invoicing Schemes

Invoice fraud,a persistent threat to businesses of all sizes,is experiencing a resurgence in sophistication and prevalence. These schemes, which involve the creation and submission of false or inflated invoices, can drain significant financial resources from unsuspecting companies.Law enforcement agencies and financial institutions are increasingly concerned about the evolving tactics employed by fraudsters, making detection and prevention more challenging than ever.

Modus Operandi: How Invoice Fraud Unfolds

The anatomy of invoice fraud typically involves several key stages. First, fraudsters create fake invoices that appear legitimate, often mimicking the branding and style of real suppliers. These invoices are then submitted to the target company’s accounts payable department. If the company lacks robust verification procedures, the fraudulent invoice may be processed and paid. The funds are then diverted to the fraudster’s account, often through a complex network of shell companies to obscure the trail.

One common tactic involves billing for services or goods that were never provided. For example, a company might receive an invoice for consulting services

or office supplies

that it never ordered or received. Another variation involves inflating the cost of legitimate services or goods. A supplier might intentionally overcharge a client, adding extra fees or expenses to the invoice.

The Economic Impact and Statistical Overview

The financial repercussions of invoice fraud are considerable. According to the Association of Certified Fraud Examiners (ACFE), invoice fraud accounts for a significant percentage of occupational fraud cases, resulting in millions of dollars in losses annually. Recent data indicates a concerning upward trend, with small and medium-sized enterprises (SMEs) being particularly vulnerable due to limited resources for fraud prevention and detection.

Invoice fraud accounts for a significant percentage of occupational fraud cases, resulting in millions of dollars in losses annually.

Association of Certified Fraud Examiners (ACFE)

Consider the case of a manufacturing company that fell victim to a sophisticated invoice fraud scheme, losing over $500,000 in a single year. The fraudsters had created fake invoices for non-existent raw materials, exploiting weaknesses in the company’s procurement process. This example underscores the importance of implementing robust internal controls and verification procedures.

Combating Invoice Fraud: Strategies for Prevention and Detection

Effective prevention and detection of invoice fraud require a multi-faceted approach. Companies should implement robust internal controls, including segregation of duties, mandatory invoice verification, and regular audits. Employee training is also crucial to raise awareness of fraud risks and empower staff to identify suspicious activity.

- Implement Segregation of Duties: Ensure that different employees are responsible for different stages of the invoice processing cycle,such as invoice creation,approval,and payment.

- Mandatory Invoice verification: Require all invoices to be verified against purchase orders and receiving reports before payment.

- Regular Audits: Conduct regular internal and external audits to identify weaknesses in internal controls and detect fraudulent activity.

- Employee Training: Provide regular training to employees on fraud prevention and detection techniques.

- utilize Technology: Implement automated invoice processing systems that can flag suspicious invoices and transactions.

Furthermore,businesses should leverage technology to enhance their fraud detection capabilities. Automated invoice processing systems can flag suspicious invoices and transactions, while data analytics tools can identify patterns and anomalies that may indicate fraudulent activity. By investing in these technologies and implementing robust internal controls, companies can significantly reduce their risk of falling victim to invoice fraud.

The Role of Law enforcement and Future Trends

Law enforcement agencies are actively investigating and prosecuting invoice fraud cases,but the complexity of these schemes often presents significant challenges. Collaboration between law enforcement, financial institutions, and businesses is essential to effectively combat this growing threat. As technology continues to evolve, fraudsters will likely develop even more sophisticated tactics, requiring ongoing vigilance and adaptation.

Looking ahead, the use of artificial intelligence (AI) and machine learning (ML) may play an increasingly significant role in both perpetrating and detecting invoice fraud. Fraudsters could use AI to create more convincing fake invoices and automate their schemes, while businesses could use AI to analyze large volumes of data and identify subtle patterns of fraud. The ongoing battle against invoice fraud will require a continuous arms race between fraudsters and those seeking to protect businesses from their schemes.

Cracking Down on Invoice Fraud: A Deep Dive into Recent Cases and Prevention Strategies

Published: by Archynetys.com

The Rising Tide of Invoice Fraud: A Global Concern

Invoice fraud,a deceptive scheme targeting businesses,continues to surge globally,posing a significant threat to financial stability. This type of fraud involves the creation and submission of fake or manipulated invoices to deceive companies into paying for goods or services that were never rendered or were misrepresented. the consequences can be devastating,ranging from substantial financial losses to reputational damage and even business closure.

According to recent data from Europol, invoice fraud has increased by approximately 30% in the last year alone, with small and medium-sized enterprises (SMEs) being particularly vulnerable. This rise is attributed to increasingly sophisticated techniques employed by fraudsters, including the use of advanced technology to create realistic-looking invoices and impersonate legitimate suppliers.

Økokrim’s Fight Against Financial Crime in Norway

In Norway, the fight against financial crime, including invoice fraud, is spearheaded by Økokrim, the Norwegian National authority for Investigation and Prosecution of economic and Environmental Crime. Økokrim plays a crucial role in investigating and prosecuting complex fraud cases, working to protect businesses and individuals from financial exploitation.

Recently, Økokrim has intensified its efforts to combat invoice fraud, launching several high-profile investigations and collaborating with international law enforcement agencies to track down perpetrators operating across borders.These efforts have led to significant arrests and the recovery of substantial sums of money defrauded from Norwegian businesses.

Case Study: Unmasking a Sophisticated Fraud Ring

One notable case involved a sophisticated fraud ring that targeted multiple businesses across Norway. the fraudsters created fake invoices for services such as “brush work” or “consulting,” often amounting to tens of thousands of Norwegian Krone (NOK). These invoices were sent to unsuspecting companies, who, due to inadequate internal controls, processed and paid them.

The investigation revealed that the fraud ring had been operating for several years, using a network of shell companies and offshore accounts to launder the proceeds of their crimes. Økokrim’s meticulous investigation, involving forensic accounting and international cooperation, ultimately led to the dismantling of the ring and the prosecution of its members.

Protecting Your Business: Practical Prevention Strategies

Given the increasing prevalence and sophistication of invoice fraud, businesses must take proactive steps to protect themselves. Implementing robust internal controls and educating employees about fraud prevention are essential.

Key Strategies for Fraud Prevention:

- Implement a multi-layered approval process: Require multiple levels of authorization for invoice payments, especially for new vendors or unusually large amounts.

- Verify vendor information: Independently verify the contact information and bank details of all vendors before making payments. Use online tools and databases to confirm their legitimacy.

- Train employees: Conduct regular training sessions to educate employees about the latest fraud techniques and how to identify suspicious invoices.

- Use technology: Implement accounting software with built-in fraud detection capabilities.These systems can flag suspicious transactions and alert you to potential problems.

- Regularly audit financial records: Conduct regular internal audits to identify any irregularities or potential fraud.

- Be wary of unsolicited invoices: Treat unsolicited invoices with extreme caution. Contact the supposed vendor directly to verify the invoice’s authenticity.

The Role of International Cooperation

Combating invoice fraud effectively requires international cooperation. Fraudsters often operate across borders, making it essential for law enforcement agencies to collaborate and share information.Organizations like Europol play a vital role in facilitating this cooperation, providing a platform for countries to share intelligence and coordinate investigations.

International cooperation is paramount in the fight against transnational financial crime. by working together, we can disrupt fraud networks and bring perpetrators to justice.

A Europol Spokesperson

Looking Ahead: The Future of Fraud Prevention

As technology continues to evolve, so too will the techniques used by fraudsters. Businesses must stay ahead of the curve by investing in advanced fraud prevention technologies and continuously updating their security protocols. Artificial intelligence (AI) and machine learning (ML) are increasingly being used to detect and prevent invoice fraud, offering promising solutions for the future.

By combining technological advancements with robust internal controls and employee education, businesses can significantly reduce their risk of becoming victims of invoice fraud and protect their financial well-being.

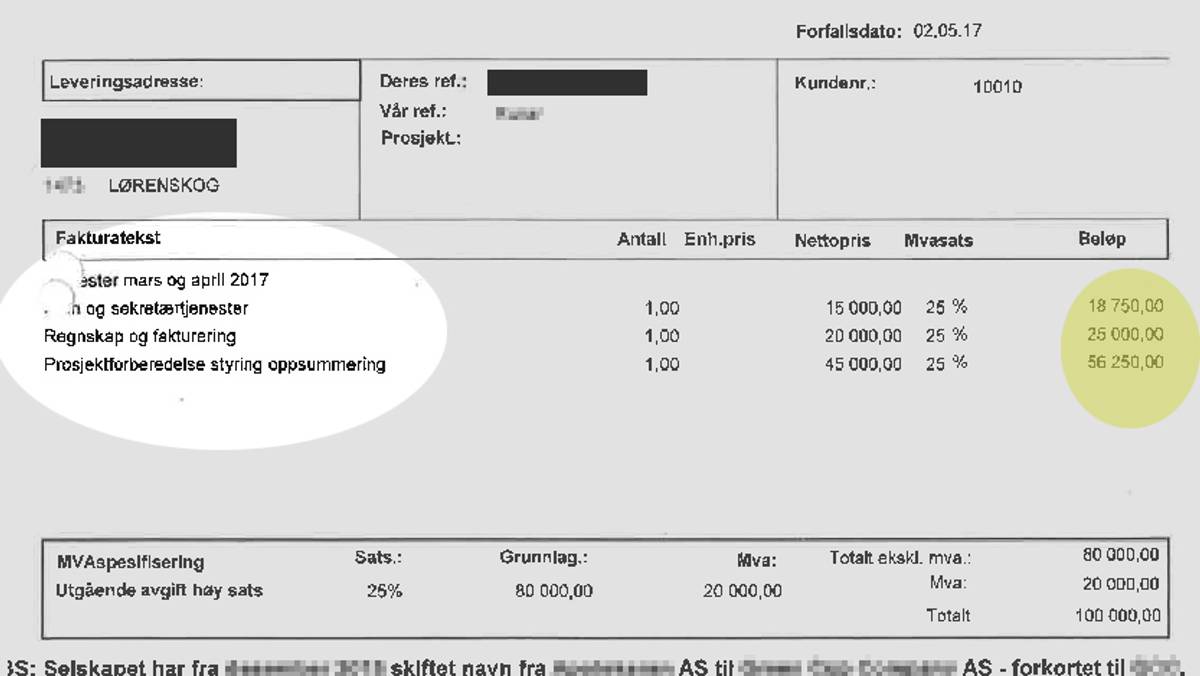

Unmasking Invoice Factories: A Deep Dive into financial Crime

By Archnetys Investigative Team

The Shadowy World of False Invoicing

In the intricate landscape of financial crime, invoice factories

represent a particularly insidious threat. These operations generate fictitious invoices for services never rendered, enabling companies to manipulate their financial records for illicit gains. The practice, while seemingly simple, has far-reaching consequences, impacting tax revenues, fair competition, and overall economic stability.

How Invoice Factories Operate

The modus operandi of an invoice factory typically involves a central figure or institution that collaborates with businesses seeking to inflate their expenses or conceal illegal activities. these businesses receive invoices for services like secretarial services, accounting, invoicing and project preparation

that were never actually provided.

According to Petter Nordeng, acting assistant head of Økokrim, the purpose of these invoices is often to cover illegal withdrawals and other crime in a company. The service involves obtaining the documentation needed for this to look legal.

The process unfolds as follows:

- The invoice factory issues a fake invoice to a company, often with a pre-agreed description of services.

- The company pays the invoice amount to the invoice factory.

- The invoice factory then transfers the funds, often through a series of accounts, back to the company, minus a commission.

The Motives Behind the Deception

Companies engage in false invoicing for a variety of reasons, primarily centered around financial gain and tax evasion. By inflating their expenses, they can:

- Reduce their taxable income, leading to lower tax payments.

- Conceal the use of undeclared labor, avoiding payroll taxes and social security contributions.

- Disguise the siphoning of funds for personal use or other illicit activities.

The consequences of these actions are significant. Tax evasion deprives governments of crucial revenue needed for public services,while unfair competition disadvantages legitimate businesses that adhere to ethical and legal standards.

A Case Study: Unveiling a Construction Industry Scheme

One recent case highlights the mechanics of an invoice factory operating within the construction industry. A man, in collusion with several construction companies, issued invoices for services that were never performed. The invoices, often labeled with generic descriptions like painting work,

were paid by the companies, with the funds then being funneled back to them through a circuitous route.

This scheme allowed the construction companies to reduce their reported profits, evade taxes, and potentially conceal the use of undocumented workers.

Combating Invoice Factories: A Multi-Faceted Approach

Addressing the problem of invoice factories requires a concerted effort from law enforcement, regulatory bodies, and businesses themselves. Key strategies include:

- Strengthening regulations and enforcement to deter false invoicing.

- Enhancing data analytics and risk assessment techniques to identify suspicious transactions.

- Promoting greater awareness among businesses about the risks and consequences of engaging with invoice factories.

- Encouraging whistleblowers to report suspected fraudulent activities.

Invoice Factory kingpin Convicted: Unpacking the Modus Operandi and Legal Fallout

The Anatomy of an Invoice Scheme

A recent case in Norway has shed light on the intricate workings of an “invoice factory,” a scheme designed to generate illicit funds through fraudulent invoicing. The individual at the centre of this operation has been convicted of both adultery and money laundering, highlighting the severity of these financial crimes.

Invoice factories, while varying in complexity, generally operate by creating fictitious invoices for goods or services that were never actually provided. These invoices are then presented to businesses,often with the promise of a kickback or other incentive for payment. The funds received are then laundered through a series of transactions to obscure their origin.

Modus Operandi: How the Scheme Unfolded

The convicted individual orchestrated a scheme involving fake invoices totaling over NOK 8 million. The process involved several key steps:

- Creating a false invoice.

- Depositing the payment into his account or cashing it out.

- returning 80% of the payment to the “customer.”

- Distributing 10% to a contact person.

- Retaining the final 10% as profit.

This distribution model highlights the collaborative nature of such schemes,involving multiple parties to facilitate the fraud and launder the ill-gotten gains.

The Legal Ramifications: Conviction and Controversy

The individual was ultimately convicted of adultery and money laundering for his role in the invoice factory operation. The total amount involved was just over NOK 8 million.

Despite admitting to the crimes, the convicted individual’s lawyer, Petter Mandt, has voiced concerns about the severity of the penalty.

He has acknowledged all criminal matters. There is no doubt about the fact in this case.

The Wider Impact of Invoice Fraud

Invoice fraud poses a significant threat to businesses and economies worldwide. According to a 2024 report by the Association of Certified Fraud Examiners (ACFE),billing schemes,which include invoice fraud,are among the most common and costly forms of occupational fraud. These schemes can lead to substantial financial losses, damage to reputation, and even business failure.

Combating invoice fraud requires a multi-faceted approach, including robust internal controls, employee training, and the use of technology to detect suspicious transactions.Businesses must also be vigilant in verifying the legitimacy of invoices and suppliers.

Looking ahead: Strengthening Financial Crime Prevention

This case serves as a stark reminder of the sophistication and potential impact of financial crimes like invoice fraud. As technology evolves, so too do the methods used by criminals to perpetrate these schemes. It is indeed crucial that law enforcement agencies, regulatory bodies, and businesses work together to stay ahead of the curve and implement effective measures to prevent and detect financial crime.

Debate Over Severity of Punishment in Adultery case involving Financial Impropriety

Published by Archnetys.com on

A recent ruling by the Borgarting Court of Appeal in Norway has sparked a debate regarding the appropriate severity of punishment in cases of adultery that involve financial impropriety. While some argue for leniency when no direct financial loss is incurred, the court has upheld a stricter sentence, drawing parallels to embezzlement.

The Core of the Controversy: Adultery vs. Financial Crime

The case revolves around a man convicted of adultery, which also involved actions deemed financially detrimental to the company against which the adultery was committed. A key point of contention is whether the punishment should be as severe as those typically reserved for direct financial crimes, such as embezzlement or fraud.

defense Argues for Leniency

The defense, led by legal representatives, contends that the two-year, five-month prison sentence is excessive. Their argument centers on the absence of direct financial loss to the company consequently of the adultery.As one representative, Mandt, stated:

We believe that the punishment is too strict because he was charged with adultery. In this adultery,there was no financial loss for the company that the adultery was made against.

This perspective suggests that the punishment should be calibrated to reflect the actual financial harm caused, rather than the act of adultery itself.

Court upholds Stricter Sentence: A Matter of Principle

Despite the defense’s arguments, the Borgarting Court of Appeal firmly rejected the appeal, maintaining the original sentence. The court’s justification highlights a broader view of financial crime and its societal impact.

The court’s reasoning, as articulated in their statement, emphasizes the potential for significant harm even when direct financial loss is not immediatly apparent:

In the Court of Appeal’s view, this form of financial crime is no less punished than draining a company for money. in both situations, business is underway that clearly contradicts the company’s interests and which is very harmful to socially.

This perspective aligns with a growing awareness of the insidious nature of financial crimes, which can erode trust, destabilize markets, and ultimately harm society as a whole. For example, the Panama Papers scandal revealed how offshore accounts, while not always illegal, can be used to conceal illicit activities and evade taxes, depriving governments of crucial revenue for public services.

Implications and Future Considerations

The court’s decision underscores the seriousness with which Norway’s legal system views actions that undermine corporate integrity, even when those actions are not explicitly defined as customary financial crimes. This case may set a precedent for future rulings involving similar circumstances, potentially impacting how adultery and related improprieties are prosecuted when they intersect with financial matters.

The debate surrounding this case highlights the complex interplay between personal conduct, corporate ethics, and the law.As financial landscapes evolve, legal systems must adapt to address emerging forms of misconduct and ensure that justice is served effectively.

Supreme Court Upholds Conviction in Fictitious Invoicing Case: A Landmark Decision

By Archnetys News Team

Strengthening the Stance Against Financial Crime

In a significant ruling, the Supreme Court has affirmed the conviction of an individual found guilty of using a corporation to lock

money through the creation of fictitious invoices. This decision underscores the judiciary’s commitment to treating financial crimes with equal severity, nonetheless of the specific methods employed.

Equivalence in Justice: Stealing from a Thief

The core principle highlighted by this verdict is that illicitly obtaining funds, whether from a legitimate business or through fraudulent means, carries the same weight under the law. As legal expert Nordeng explains, locking money through a corporation by creating fictitious invoices should be punished as strictly as when an otherwise legal business taps for money.

This perspective emphasizes that the act of defrauding, regardless of the victim’s own ethical standing, constitutes a serious offence.

It will be in a way that you say it is indeed just as serious if you steal from a thief,as if you are taking the money from a company that is a legal business.

The Legal Journey: From Initial Conviction to Supreme Court Rejection

Following the initial conviction,the defendant pursued appeals through the Borgarting Court of Appeal,which were later rejected. The case then reached the supreme Court,which has now also denied the appeal,effectively solidifying the original judgment.This lengthy legal process demonstrates the thoroughness with which the courts examined the case and the evidence presented.

Implications for Corporate Financial Practices

This ruling serves as a stark warning to individuals and businesses contemplating similar schemes. The creation of fictitious invoices, a common tactic in financial fraud, will be met with stringent legal consequences. According to recent statistics from the Financial Crimes Enforcement Network (FinCEN), cases involving fraudulent invoicing have increased by 15% in the last year, highlighting the urgency of addressing this issue.

Expert commentary

attorney Petter Mandt provided insights into how he and his client are assessing the verdict. While specific details of their assessment remain confidential, it is clear that the ruling has significant implications for future legal strategies in similar cases.

Looking Ahead: Reinforcing Financial Integrity

The supreme Court’s decision sends a clear message: financial manipulation and fraud will not be tolerated. This landmark ruling is expected to have a deterrent effect, encouraging greater transparency and accountability in corporate financial practices. Continued vigilance and robust enforcement are crucial to maintaining the integrity of the financial system.

The rise of Professionalized Financial Crime

Law enforcement agencies are expressing growing concern over the increasing sophistication and professionalization of money laundering operations. These schemes often utilize legitimate business structures and regulatory loopholes to conceal illicit activities, making detection exceedingly difficult.

According to Økokrim, the norwegian National Authority for Investigation and Prosecution of Economic and environmental Crime, the complexity of these operations is a major challenge. Criminals are adept at exploiting legal frameworks to mask the true nature of their transactions.

False invoicing: A Key Tactic

one particularly worrying trend is the use of false invoicing to disguise the distribution of criminal proceeds. This involves creating fake invoices to make it appear as though legitimate business transactions are taking place, when in reality, the money is being laundered.

We are concerned because we see that this has begun to be professionalized.Statement from Nordeng, law enforcement official

This method allows criminals to inject illicit funds into the financial system, making it difficult to trace the origin of the money. the scale and frequency of these activities are causing significant alarm among authorities.

The Engine of Crime: Why money Laundering Matters

Authorities emphasize that money laundering is not a victimless crime. It serves as the very engine that fuels a wide range of criminal activities, from drug trafficking and terrorism to fraud and corruption. By cleaning illicit funds,criminals are able to profit from their crimes and continue to operate with impunity.

We are very concerned about both the spread and the increase because, money laundering is the very engine of the crime.Statement from Nordeng, law enforcement official

The United Nations Office on Drugs and Crime (UNODC) estimates that between 2% and 5% of global GDP, or $800 billion to $2 trillion, is laundered each year. This staggering figure highlights the scale of the problem and the urgent need for effective countermeasures.

Combating the Threat: A Multi-faceted Approach

Addressing the growing threat of sophisticated money laundering requires a multi-faceted approach. This includes strengthening regulatory frameworks, enhancing international cooperation, and investing in advanced technologies to detect and prevent illicit financial flows. Law enforcement agencies are working to improve their ability to identify and prosecute those involved in these schemes.