“`html

IP Co-branding in the Food Industry: A deep Dive into 2025 Trends

Table of Contents

The Rise of IP co-branding: More Than Just a Fad?

In today’s saturated consumer market, IP co-branding has become a ubiquitous strategy. From toys and theme parks to food, fashion, and even technology, brands are increasingly leveraging the power of intellectual property to capture consumer attention. However,beneath the surface of seemingly simple collaborations lies a complex web of considerations.

While the allure of speedy profits is strong,successful IP co-branding demands a deep understanding of the IP itself,its associated culture,and the intricate rules and values of its fanbase. Missteps can lead to consumer backlash and reinforce the perception of IP co-branding as a short-term gimmick with limited long-term value.the challenge now is to evolve these partnerships from fleeting marketing campaigns into lasting, value-driven strategies that revitalize both brands and IPs.

Food and Beverage lead the Charge: A Q1 2025 Analysis

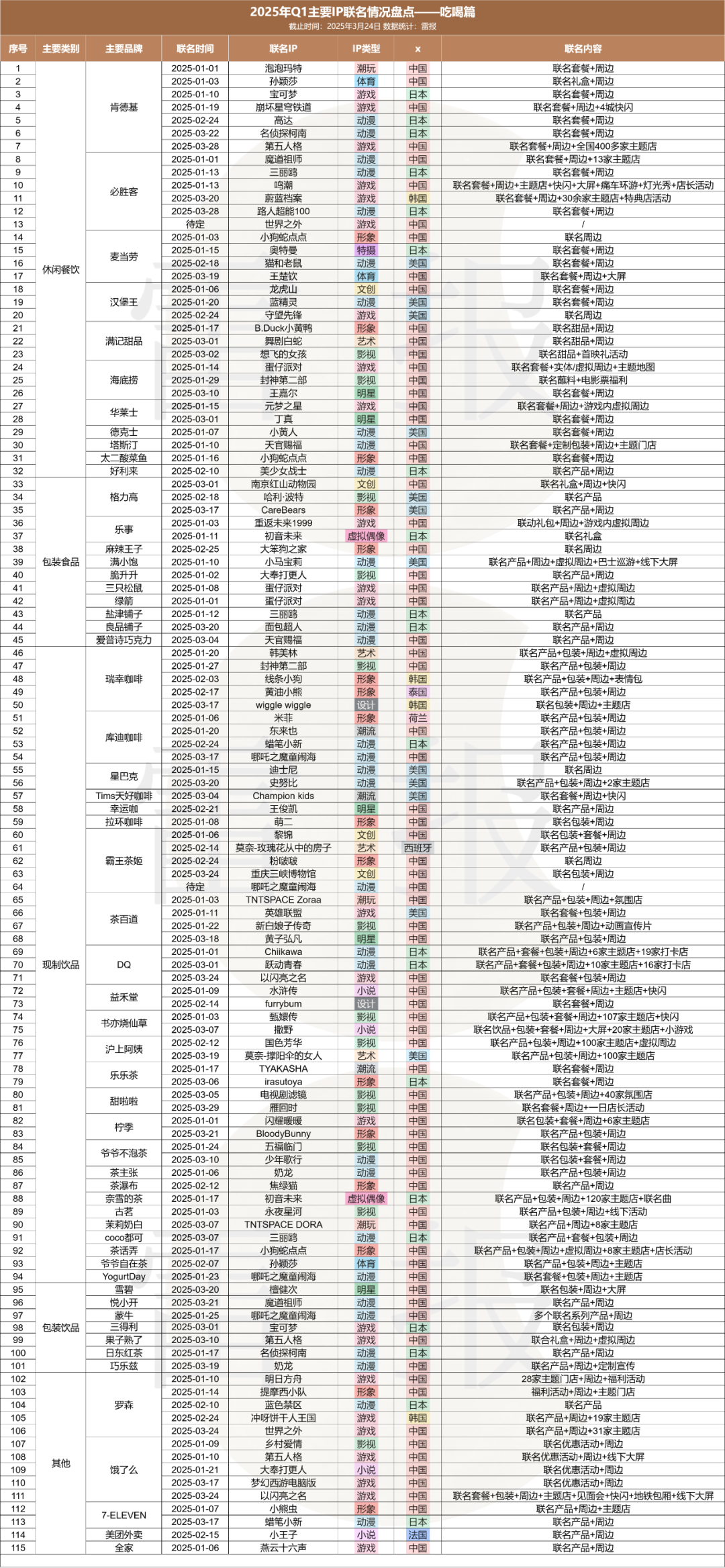

The food and beverage sector, notably fast food, snacks, and freshly prepared drinks, stands out as a leader in IP co-branding. To gain insights into the current state and future direction of this trend, Archnetys news analyzed 115 IP co-branding initiatives within the food and beverage industry during the frist quarter of 2025, drawing from financial reports and online data.

Q1 2025: A Feast of Collaborations

Why the Food Industry Remains Hooked on IP Co-branding

Our research identified 115 IP co-branding events in the food and beverage sector during Q1 2025, involving 58 brands and 92 IPs. The data reveals a clear preference for certain types of collaborations.

Freshly made beverages (e.g., Luckin Coffee, Cha Baidao) accounted for approximately 43% of these collaborations, followed by casual dining (e.g., KFC, Pizza Hut) at 28%. Packaged foods and beverages represented smaller portions, while retail channel brands like Quanjia and Luosen contributed the remainder.

The dominance of freshly made beverages and casual dining, totaling 70% of all collaborations, highlights the appeal of these categories. Their inherent necessity, high consumption frequency, convenient accessibility, affordable pricing, and strong brand recognition make them ideal candidates for successful IP co-branding.

Success Stories and Rising Costs

The potential rewards of successful IP co-branding are evident in several recent campaigns. For example,KFC’s collaboration with table tennis star Sun Yingsha saw 500,000 packages sold within two and a half hours,generating over 34.5 million yuan in revenue. Similarly, Kudi Coffee’s partnership with “Nezha: The Devil Child’s Stirring” achieved impressive sales on Meituan and Douyin platforms, exceeding hundreds of thousands of units.

Luckin Coffee, a prolific collaborator, launched 34 IP co-branding campaigns last year, generating meaningful buzz online. The “Black Myth” collaboration saw 400,000 limited-edition posters sell out instantly, while the “Line Puppy” and “Butter Bear” collaborations resulted in millions of cups sold within their first weeks.

however, these successes come at a cost. Licensing fees for popular IPs like “Nezha: The Devil Child’s trouble” have reportedly soared, raising concerns about the profitability of these ventures. Furthermore,marketing expenses for companies engaging in IP co-branding are on the rise. Luckin’s 2024 financial report reveals a 43.5% year-over-year increase in sales and marketing expenses, while newly listed companies like Gu Ming and Mixue Bingcheng have also reported significant increases.

The frequency of collaborations also varies among brands.While some brands engage in multiple partnerships per month, others only participate once per quarter, suggesting different approaches to IP co-branding strategies.

The timing of collaborations also appears to be influenced by seasonal factors, with January seeing the highest number of initiatives and February experiencing a dip due to the Spring Festival holiday.

The Most Sought-After IPs: A Battle for Brand Association

Popular IP Categories and Nationalities

From an IP viewpoint, animation, games, and image-based IPs are the most popular choices for brands. Film and television IPs also rank highly,while other categories like celebrities,art,and sports have a smaller presence.

Domestic IPs dominate the IP co-branding landscape, accounting for the majority of collaborations. Japanese IPs hold the second position,followed by american IPs. This suggests that cultural proximity,policy compliance,audience familiarity,and cost considerations favor domestic IPs in the Chinese market.

Specifically, domestic game IPs, Japanese animation IPs, domestic film and television IPs, domestic image IPs, domestic animation IPs, and American animation IPs are the most sought-after categories for food and beverage co-branding in Q1 2025.

Deep Integration: The Rise of Game IP Collaborations

Domestic game IPs stand out for their deep integration into co-branding campaigns. Beyond product tie-ins,these collaborations frequently enough involve in-game content,offline events,and themed stores,creating a extensive brand experience.