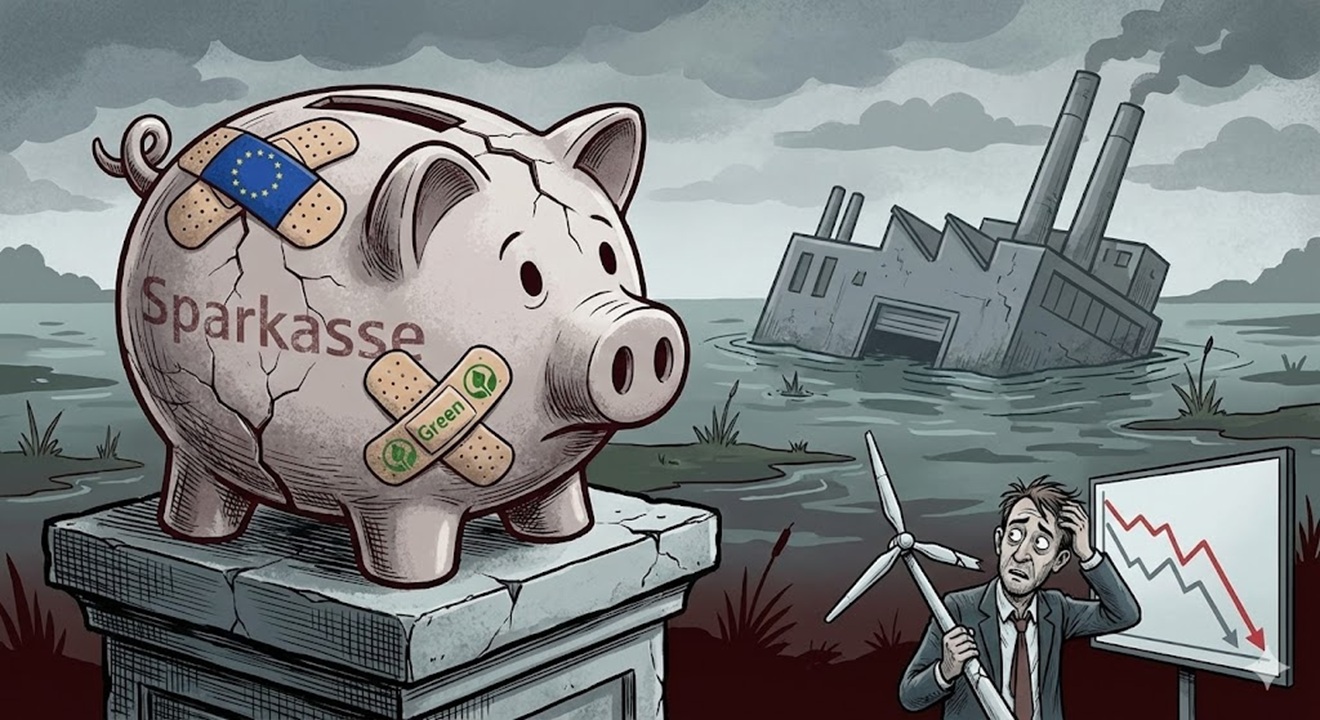

The crisis in the German real economy is infecting bank balance sheets. While the giants celebrate, the connective tissue of the Sparkasse and cooperative banks is buckling under the weight of the failures of the Mittelstand.

2025 ends like a a terrible year for the German economy, a disaster that can no longer be hidden under the carpet of pro-European rhetoric. The numbers speak clearly and are scary: around 24,000 companies have declared insolvency. To find a worse figure we have to go back more than twenty years, to 2003, when the bursting of the dot-com bubble and the subsequent recession led to the bankruptcy of 39,000 companies.

But this time it’s different. It’s not a speculative bubble bursting, it’s the very structure of the German production system that is crumbling.

Deindustrialization and impaired loans: the bill reaches the bank

Table of Contents

Loan defaults in the last year are estimated at around 57 billion euros. A monstrous figure that strikes directly at the heart of the local banking system. Why? Because the famous middle class German – the backbone of European manufacturing – is financed 40% through savings banks (Savings banks) and 25% through cooperative banks (Volksbanken).

The causes are known, even if Brussels pretends not to see them: a toxic mix of hyper-regulation, a deindustrialization forced by fanatical climate policy, a self-inflicted energy crisis and an unsustainable fiscal burden. This poisonous cocktail depressed domestic demand and made production in Germany uncompetitive.

The 20% drop in industrial production isn’t just a cold statistic. It means that the related industries, suppliers and services are falling like dominoes. And guess who will pay the bill for these never repaid loans?

Pressure below the surface: Deutsche Bank‘s trick isn’t enough

At first superficial glance, some might say that the banking sector is holding up. Deutsche Bank increased profits, sure. But that is international finance. The reality in the area is very different.

Cooperative banks (Volks- and Raiffeisenbanken) have already seen a 25% drop in profits last year, and 2025 promises to be worse. Germany’s three-pillar model (private banks, public institutions and cooperatives) is showing deep cracks. Years of zero rates have crushed margins, and now the sudden reversal in rates, combined with the recession, is crushing both businesses and families.

The disaster of “Politically Correct” investments

There is an even more disturbing aspect: the perverse intertwining between cooperative banks and politics. Let’s take the case of BayWaa Bavarian agricultural cooperative that almost went bankrupt after embarking on global investments in renewable energy, leaving a gaping hole 100 million euros.

It is the perfect example of the risks of economic dirigism: billions channeled towards the “climate economy” through state guarantees (KfW) to keep alive a zombie economy that the free market would have already wiped out. Other examples multiply:

- VR Bank Dortmund Northwest: losses of 280 million on risky real estate funds.

- VR bench Bad Salzungen-Schmalkalden: saved by the protection fund after similar real estate disasters.

Banks, seeing traditional business collapse with healthy companies, have moved towards high-risk investments in search of profits. Result? A disaster. BaFin analysis shows that non-performing loans increased by 25% in a year, reaching 36.5 billion euros.

Branches closed and Credit Crunch on the horizon

Banks are reacting the only way they know how: by cutting. Over 1,000 branches close each year. There Savings Bank local, once a pillar of the community, is disappearing, leaving artisans and small businesses without a direct interlocutor.

We are faced with the paradox of current monetary policy. The ECB may start cutting rates (belatedly), but if banks have balance sheets full of bad loans and capital blocked by provisions, credit to the real economy stops. Unless Germany radically changes political and energy direction – an unlikely scenario with the current ruling class – we are in for a credit crunch that will further accelerate the recessionary spiral. Austerity and ideological choices are taking their toll, and it will be very high.

Illustrative image

Questions and answers

What is the difference between the crisis of the big banks and that of the local German banks?

Large banks such as Deutsche Bank operate globally and have diversified their revenues (investment banking, asset management), managing to maintain positive profits. Local banks (Savings banks and cooperatives), however, are almost totally exposed to the German real economy (SMEs and mortgages). If the middle class and real estate collapse due to the internal recession, these banks absorb the blow directly, having no international “shock absorbers”.

Are German savers at risk of losing their deposits?

In the immediate future, the direct risk on deposits under 100,000 euros is low thanks to guarantee systems (such as the BVR for cooperatives). However, the protection system is based on the overall strength of the sector. If failures become systemic and too many banks require simultaneous bailouts, guarantee funds could come under stress, possibly requiring state intervention (bail-out), which would end up weighing on taxpayers.

Why aren’t ECB rates helping the situation?

Because we are in a classic liquidity trap or, worse, a solvency crisis. Even if the ECB lowers rates, banks will not willingly lend money to an economy in recession with companies failing at a record rate. Additionally, banks must set aside capital to cover losses on existing loans, further reducing their ability to provide new credit. It is a problem of a “broken economic engine”, not just of “petrol” (rates).

FOLLOW